Health Insurance in Thailand: What I’ve Understood, What I’m Still Looking For

by Mário Ferreira | 2026 | Health & Insurance

✍️ Transparency note: this article is different from the other guides on this blog. I have not yet found a health insurance solution that fully suits me. I share here my analysis, research and hesitations — as they are. If you have found a solution, your comments are invaluable. My situation is a little particular: I hold a spouse visa (Non-Immigrant O, known as the ‘Thai Wife visa’), which does not impose mandatory health insurance — unlike the O-A retirement visa. I am therefore not legally required to have one. This does not mean I consider the risk negligible — quite the contrary. But it explains why I am taking the time to choose carefully rather than subscribing hastily to meet an administrative obligation.

Health insurance is without doubt the most important — and most complicated — subject for a European expat settling in Thailand. It is not just a question of money. It is a question of real security in the face of a healthcare system one does not know.

I have analysed several options — SafetyWing, Cigna Global, AXA, Allianz Care, and a local Thai insurer (Aya). I have not yet decided. Here is why.

1. What the Retirement Visa Requires

The Non-Immigrant O-A visa imposes mandatory health insurance. Minimum requirements:

- Inpatient (IPD) coverage: 400,000 THB minimum

- Outpatient (OPD) coverage: 40,000 THB minimum

- Recommended total coverage for peace of mind: 100,000 USD

- Insurer must be listed on longstay.tgia.org. Since October 2021, the required total coverage is 3,000,000 THB or 100,000 USD per year (COVID-19 included). Some consulates still apply the old system — always verify with your local consulate.

- An official Foreign Insurance Certificate must be issued, signed and stamped by the insurer

⚠️ The legal minimum is deliberately low. In practice, a serious hospitalisation in a Thai private hospital can quickly exceed 500,000 THB. Do not settle for the minimum.

🚑 Medical evacuation to another country is not covered by the legal minimum. This is a criterion I consider essential — and one that considerably complicates the choice.

2. The Options I Have Analysed

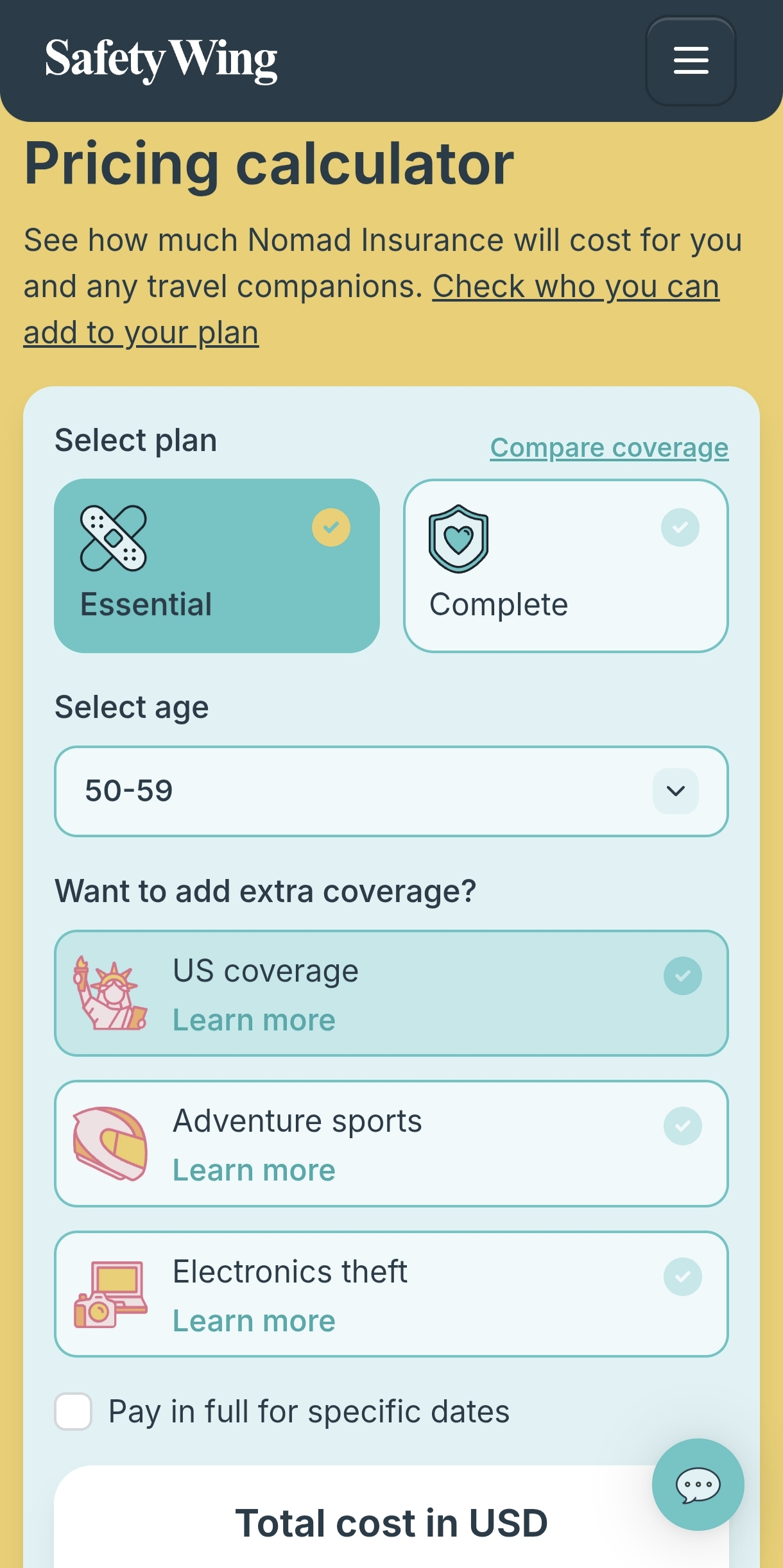

SafetyWing — Nomad Insurance

This is the most accessible option in terms of cost and simplicity. Monthly payment with no commitment, online subscription in a few minutes.

- Strengths: price, flexibility, simple subscription, international coverage

- Weaknesses: limited basic coverage, fairly low caps on some benefits and medical evacuation not systematically included in all plans

- Retirement visa acceptance: yes, if the chosen plan meets the required thresholds

🏥 SafetyWing — Flexible and accessible option. Check that the chosen plan covers the retirement visa requirements. → See pricing

Cigna Global

One of the references for expats. Solid coverage, international network and medical evacuation available. But the price rises quickly after 50.

- Strengths: very complete coverage, medical evacuation and a hospital network in Thailand

- Weaknesses: high price for over-55s, pre-existing condition exclusions sometimes restrictive

- Retirement visa acceptance: yes

AXA

AXA offers specific plans for expats with international coverage. Customer service quality varies by country. The application procedure is more complex.

- Strengths: recognised European brand, solid coverage

- Weaknesses: heavy subscription process, high price after 50

Allianz Care

Similar to Cigna and AXA in terms of positioning. Premium international coverage. Premium price too.

- Strengths: very broad coverage, medical evacuation included

- Weaknesses: high cost, complex subscription

Aya Insurance — The Local Thai Option

Aya is a Thai insurer offering plans at significantly lower prices than international insurers. It is the solution used by many long-term expats in Thailand.

- Strengths: very competitive prices, accepted for retirement visa, knowledge of the Thai hospital system

- Weaknesses: coverage limited to care in Thailand, international medical evacuation not included in basic plans, documents and procedures in Thai or basic English

💡 Aya is very popular among long-term expats who do not plan to travel frequently outside Thailand. For those who return regularly to Europe, international coverage becomes indispensable.

3. Comparison Table

| Insurer | Price approx. 50–59 | Evacuation | Ret. visa | Complexity |

|---|---|---|---|---|

| SafetyWing | ~161 $/mois (Essential) | ⚠️ By plan | ✅ | Easy |

| Aya Insurance | ~40–80 €/mois | ❌ Base | ✅ | Medium |

| Cigna Global | ~200–400 €/mois | ✅ | ✅ | High |

| AXA | ~180–350 €/mois | ✅ | ✅ | High |

| Allianz Care | ~200–400 €/mois | ✅ | ✅ | High |

⚠️ Prices shown are estimates. They vary considerably depending on age, medical history and chosen coverage level. Always request a personalised quote.

4. The Obstacles I Encountered

The Price After 50

This is the first wall. Quality international insurers (Cigna, AXA, Allianz) have premiums that explode after 55–60. What costs €150/month at 50 can easily reach €300–400/month at 60 — a considerable budget item.

Pre-existing Condition Exclusions

All expat health insurers have exclusion clauses for pre-existing conditions. Hypertension, diabetes, cardiac problems — anything diagnosed before subscription can be excluded or loaded. For European retirees over 55, this is often a real obstacle.

Medical Evacuation — My Non-Negotiable Criterion

I live in a rural Isaan village. Surin hospital is decent, but for a serious emergency, Bangkok or even repatriation to Europe may be necessary. International medical evacuation is only included in premium plans — and that is precisely where prices become prohibitive.

✍️ My current situation: I am without specific expat health insurance at this time. I am aware this is a risk. I continue to analyse the options. This is not a situation I recommend — it is simply the reality I share.

5. What I Recommend Nevertheless

Even without having decided for myself, here is what I would advise someone arriving in Thailand:

- Don’t come without minimum coverage. Even a basic SafetyWing plan is better than nothing.

- Check that your insurer is listed on longstay.tgia.org before subscribing.

- Declare your medical history honestly — a false declaration can invalidate the entire contract.

- If you are under 55 and in good health, Cigna or AXA remain accessible at a reasonable cost.

- If the budget is tight, Aya Insurance is a viable option for care in Thailand — supplemented by a separate evacuation plan if necessary.

- Ask about public hospitals: the 30-baht health card is not accessible to foreigners, but public hospitals accept foreigners with direct payment, at significantly lower rates than private hospitals.

🏥 SafetyWing — The most accessible option to start. Check the caps for your situation. → See pricing

6. What I Expect from You

This article is deliberately incomplete — because my thinking is incomplete. If you are an expat in Thailand and have found a solution that suits you, your feedback is invaluable.

Questions I am particularly interested in:

- Have you taken out Aya Insurance? How does reimbursement work in practice?

- Do you have a separate medical evacuation solution?

- How did you handle pre-existing condition exclusions?

- Are there insurers I have not mentioned that deserve attention?

🔄 This article will be updated as soon as I have decided for myself. I will publish my complete personal experience, with the concrete details of subscription, cost and coverage.

— Mário Ferreira | Surin, Isaan, Thailand

💬 Found a suitable health insurance in Thailand? Share your experience in the comments — you’ll help the whole community!

📌 Also read: our complete Thailand Retirement Visa guide and the mandatory insurance conditions.

Pingback: A Hospital Far, Far Away…

Pingback: Um hospital longe, longe…